Pyharmonics documentation

Pyharmonics detects harmonic patterns in OHLC candle data for any stock or crypto asset. See Scott Carney’s books at harmonictrader.com for more information on harmonic patterns and follow author Scott Carney yourself.

A video tutorial https://www.youtube.com/watch?v=oLPU_f7AiGE will walk you through installation.

Installation

I recommend using a virtual env.

From git

$ git clone git@github.com:niall-oc/pyharmonics.git

$ cd pyharmonics

$ pip install .

$ cd src

$ python

>>> from pyharmonics.marketdata import BinanceCandleData

From pypi

$ pip install pyharmonics

$ python

>>> from pyharmonics.marketdata import BinanceCandleData

The guides below provide code snippets. For a full spec of the API click on the `src` link at the bottom of the table of contents.

Mini Guide

Use the market data features or generate your own market data matching the dataframe schema below. close_time, dts can be omitted

1>>> from pyharmonics.marketdata import BinanceCandleData

2>>> b = BinanceCandleData()

3>>> b.get_candles('BTCUSDT', b.MIN_15, 1000)

4>>> b.df

5>>> b.df

6 open high low close volume close_time dts

7index

82023-07-09 07:44:59+01:00 30249.04 30267.04 30233.79 30262.33 79.71611 1688885099 2023-07-09 07:44:59+01:00

92023-07-09 07:59:59+01:00 30262.32 30267.87 30235.00 30254.79 136.31718 1688885999 2023-07-09 07:59:59+01:00

102023-07-09 08:14:59+01:00 30254.80 30283.50 30233.33 30283.50 185.04086 1688886899 2023-07-09 08:14:59+01:00

112023-07-09 08:29:59+01:00 30283.50 30283.50 30263.37 30263.37 74.17937 1688887799 2023-07-09 08:29:59+01:00

122023-07-09 08:44:59+01:00 30263.37 30270.09 30243.10 30257.30 121.15791 1688888699 2023-07-09 08:44:59+01:00

13... ... ... ... ... ... ... ...

142023-07-19 16:29:59+01:00 29841.37 29902.00 29841.36 29878.00 267.42077 1689780599 2023-07-19 16:29:59+01:00

152023-07-19 16:44:59+01:00 29878.00 29933.00 29866.15 29890.01 245.03318 1689781499 2023-07-19 16:44:59+01:00

162023-07-19 16:59:59+01:00 29890.01 29995.16 29890.00 29956.46 611.16786 1689782399 2023-07-19 16:59:59+01:00

172023-07-19 17:14:59+01:00 29956.46 29979.00 29901.70 29930.57 365.35485 1689783299 2023-07-19 17:14:59+01:00

182023-07-19 17:29:59+01:00 29930.57 29930.57 29870.00 29901.40 244.14513 1689784199 2023-07-19 17:29:59+01:00

19

20[1000 rows x 7 columns]

Create a technicals object for further analysis.

1>>> from pyharmonics.technicals import Technicals

2>>> t = Technicals(b.df, b.symbol, b.interval)

Search for a harmonic pattern.

1>>> from pyharmonics.search import HarmonicSearch

2>>> m = HarmonicSearch(t)

3>>> m.search()

Plot the findings.

1>>> from pyharmonics.plotter import Plotter

2>>> p = Plotter(t, 'BTCUSDT', b.MIN_15)

3>>> p.add_harmonic_plots(m.get_patterns(family=m.XABCD))

4>>> p.show()

You will see something like this.

See all harmonic patterns.

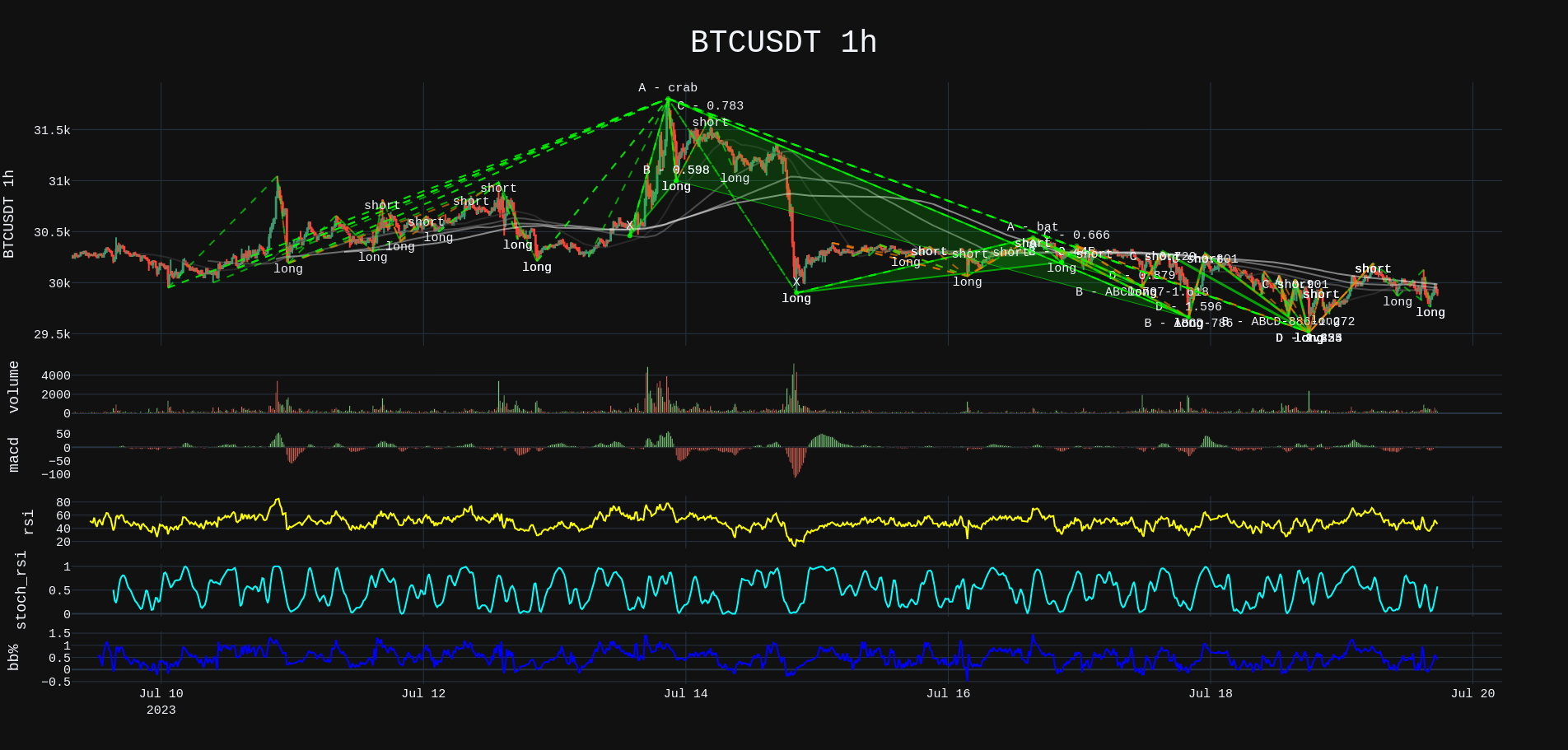

1>>> p = Plotter(t, 'BTCUSDT', b.HOUR_1)

2>>> p.add_harmonic_plots(m.get_patterns())

3>>> p.show()

You will see something like this.

See all forming patterns.

1>>> h = HarmonicSearch(t)

2>>> h.forming()

3>>> p = Plotter(t, 'BTCUSDT', b.HOUR_1)

4>>> p.add_harmonic_plots(h.get_patterns(formed=False))

5>>> p.show()

etc.